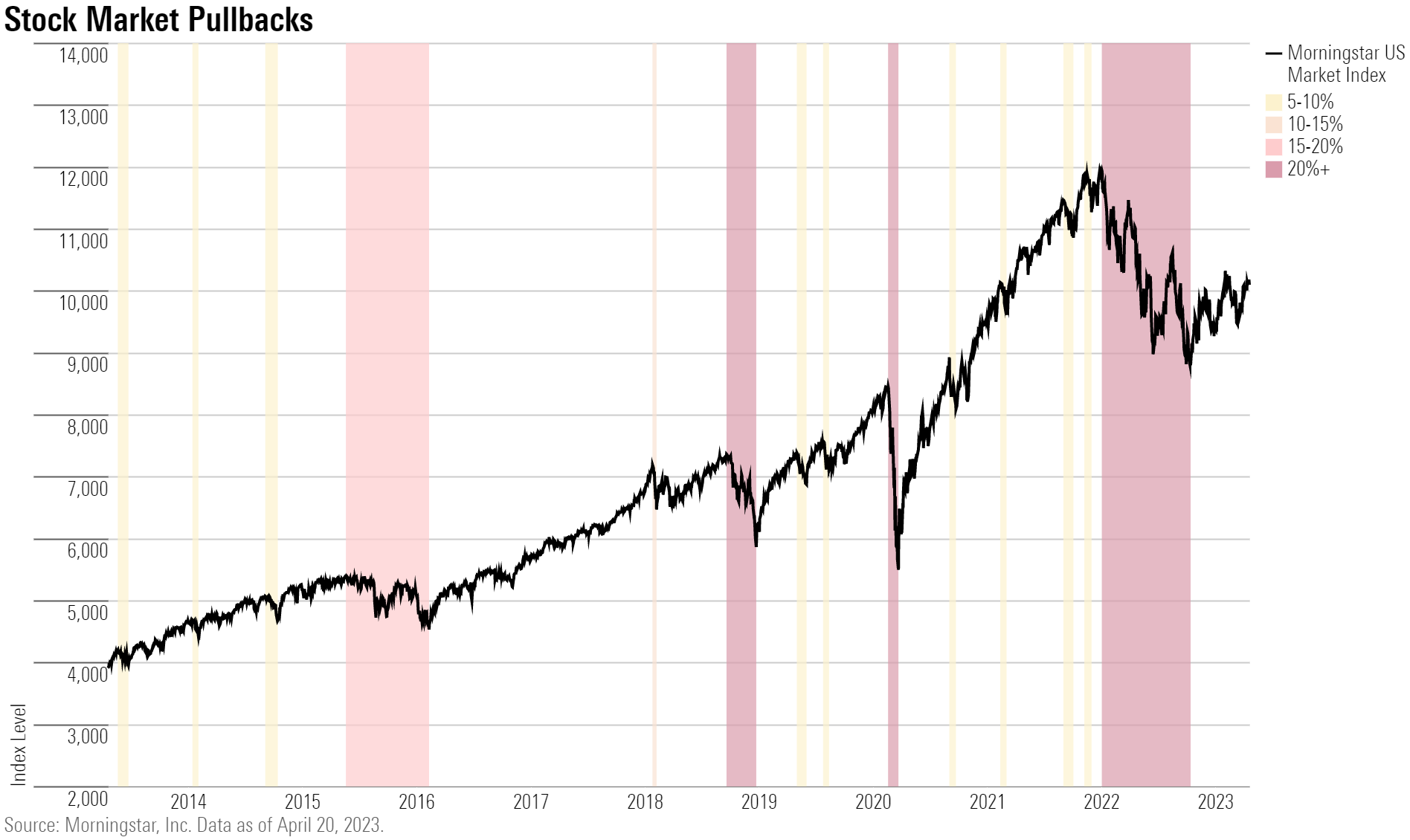

Equity markets operate on a fundamental paradox: long-term appreciation is functionally funded by short-term instability. The S&P 500 experiences 1% and 2% daily drawdowns with high historical frequency, yet these events are often mischaracterized as systemic threats rather than standard operational overhead. To treat a single-day 2% drop as an anomaly is to ignore the historical distribution of returns. An investor’s ability to capture the equity risk premium depends entirely on their capacity to distinguish between stochastic noise and structural shifts.

The Frequency Distribution of Market Turbulence

Volatility is not a defect of the modern financial system; it is a core feature of price discovery. The S&P 500 has historically experienced 1% daily declines multiple times per month and 2% drops several times per year. These are not black swan events. They are the "rent" paid for the compounding growth of the asset class. Also making news in this space: The Cuban Oil Gambit Why Trump’s Private Sector Green Light is a Death Sentence for Havana’s Old Guard.

The primary failure in retail investor psychology stems from a misunderstanding of Expected Value ($EV$). When a portfolio drops 2% in eight hours, the visceral reaction is to mitigate further loss. However, the probability of a subsequent 2% drop the following day does not increase linearly with the first. Market history suggests that these sessions often cluster, but they rarely signal a terminal collapse of the underlying index.

A 1% drop in the S&P 500 represents a recalibration of sentiment or a reaction to specific macroeconomic data points—often interest rate projections or employment figures. At this scale, the movement is almost entirely driven by high-frequency trading algorithms and institutional rebalancing. It lacks the momentum required to break long-term trend lines. Additional details into this topic are detailed by The Wall Street Journal.

The Three Pillars of Volatility Management

Navigating daily fluctuations requires a transition from emotional reaction to a mechanical framework. Professional capital allocators do not "hope" the market stays flat; they build systems that assume it will not.

1. The Cost of Re-Entry

Selling during a 2% drawdown introduces Execution Risk. The most significant upward price movements often occur within days of the sharpest downward movements. Missing the ten best days in a decade of trading can reduce total returns by over 50%. The math is unforgiving: the cost of being "out" of the market during a recovery is significantly higher than the temporary pain of a daily dip.

2. Time Horizon as a Risk Sink

Risk is a function of time. Over a 24-hour period, the S&P 500 is essentially a coin flip, with a slight bias toward the upside. Over a 20-year period, the probability of a negative return on the S&P 500 approaches zero based on historical data. Short-term volatility is the mechanism that filters out "weak hands"—investors who have mismatched their liquidity needs with their asset duration.

3. The Rebalancing Trigger

For a disciplined investor, a 2% drop is a signal for automated rebalancing. If a target allocation is 60% equities and 40% bonds, a sharp equity drop pushes the ratio toward the defensive side. Systematic investors use this as a mechanical prompt to sell bonds and buy equities at a lower cost basis. This removes the "choice" from the process, replacing anxiety with an algorithm.

Structural Cause and Effect: Why the 2% Drop Happens

To ignore a drop, one must first understand what causes it. Most 1% to 2% daily declines are the result of three specific catalysts that do not inherently alter the value of the underlying companies.

- Liquidity Cascades: When a specific price level is breached, stop-loss orders are triggered at scale. This creates a temporary vacuum of buyers, causing the price to gap down. This is a technical event, not a fundamental one.

- Multiple Compression: If the Federal Reserve signals a "higher for longer" stance on interest rates, the Discounted Cash Flow (DCF) models used by analysts must be adjusted. The future earnings of the S&P 500 become less valuable in present-dollar terms, leading to an immediate, one-time repricing.

- Information Asymmetry: Large-scale institutional investors often move in "blocks." A single pension fund rebalancing its billions out of tech and into healthcare can move the entire index for a day. Retail investors who sell in response to this are essentially providing liquidity to the institutions they are trying to emulate.

The Mathematical Reality of Recovery

The recovery from a 1% or 2% drop is statistically probable within a short window, provided the broader economic cycle remains in an expansionary phase. The core risk is not the 2% drop itself, but the Permanent Impairment of Capital. This occurs only if an investor sells at the bottom or if the underlying companies go bankrupt.

Given that the S&P 500 is a cap-weighted index of the largest American corporations, the bankruptcy of the entire index is a near-impossible scenario without a total collapse of the global trade infrastructure. Therefore, "volatility" and "risk" are often used interchangeably, but they are distinct concepts. Volatility is the price variance; Risk is the permanent loss of money.

Implementing the Strategic Buffer

To successfully "shrug off" daily drops, an investor must have a pre-defined Liquidity Buffer. This is the capital held in cash or cash equivalents (like Treasury bills) that covers 6 to 24 months of living expenses.

The existence of this buffer changes the psychology of the investor. When the market drops 2%, the investor does not fear for their ability to pay rent or buy groceries. Their "survival" is decoupled from the daily ticker. This allows the equity portion of the portfolio to remain aggressive and volatile, maximizing long-term compounding while the cash buffer handles short-term stability.

Tactical Response Framework for Market Declines

When a 2% drop occurs, the following diagnostic steps should be taken:

- Check the VIX: If the CBOE Volatility Index (VIX) is spiking but remains under 30, the movement is likely standard corrective behavior.

- Verify the Narrative: Is the drop caused by a systemic failure (e.g., 2008 banking crisis) or a standard macro adjustment (e.g., a slightly higher inflation print)? Most 2% drops fall into the latter category.

- Evaluate Portfolio Drift: Determine how much the daily drop has moved your actual allocation away from your target. If the drift is less than 5%, no action is required.

- Tax-Loss Harvesting: In a taxable account, a sharp drop can be used to sell losing positions to offset future capital gains, while immediately buying a similar (but not identical) ETF to remain in the market. This turns a market "loss" into a tax asset.

The most sophisticated approach to a 2% market drop is to treat it as a non-event. The energy spent analyzing a single day’s movement is almost always wasted. The focus should remain on the aggregate earnings growth of the S&P 500 companies, which historically trends upward regardless of the noise of any specific Tuesday afternoon.

Maintain the target allocation. Reinvest dividends automatically. Allow the mathematical certainty of compounding to outweigh the temporary discomfort of the daily chart. The only way to lose in a 2% drop is to participate in the panic that caused it.