Arthur Vance spent forty-two years tracking numbers that didn't belong to him. As a mid-level accountant in Ohio, his days were measured in spreadsheets, the satisfying click of a mechanical calculator, and the steady, quiet growth of his own 401(k). He wasn't rich. But he was disciplined. Every month, a portion of his paycheck vanished into the market, compounding in the dark, earmarked for a future he wasn't entirely sure he would live to see.

When he finally retired, the numbers ceased to be abstract. They became his life support. Learn more on a connected topic: this related article.

But Arthur had a problem that didn't fit neatly into a spreadsheet. His wife, Martha, had passed away three years before his retirement, after a long battle with illness that was softened only by the extraordinary care of a local, donor-funded hospice center. In the quiet months that followed, Arthur found his purpose not in golfing or traveling, but in giving back. He wanted to channel his remaining wealth into that same hospice, ensuring other families found the same dignity in their darkest hours.

That was when he hit the wall. Further reporting by ELLE delves into related perspectives on this issue.

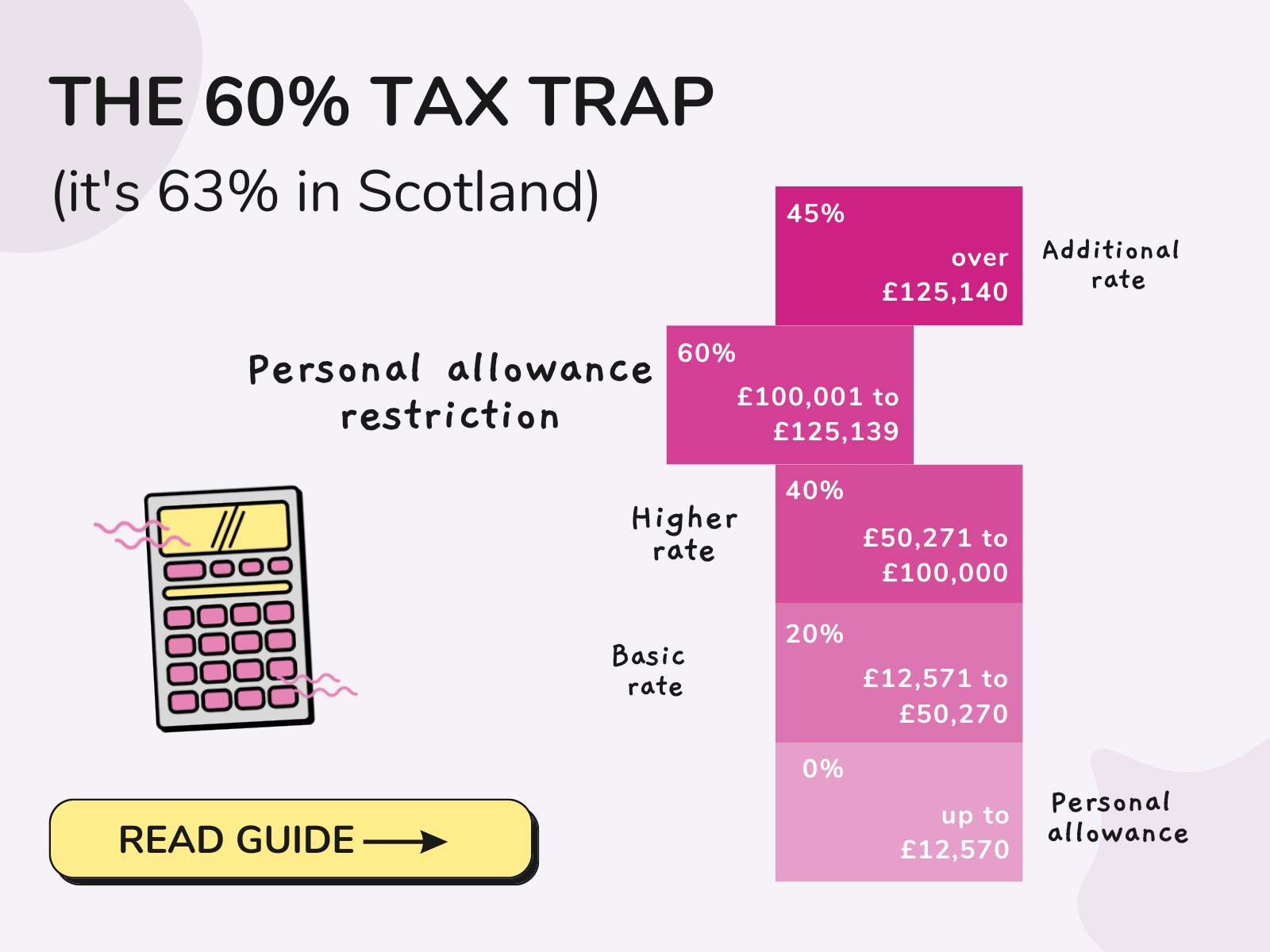

To give that money away, Arthur first had to take it out. Because his savings were locked in a traditional 401(k), every dollar he withdrew to hand to the hospice was treated by the government as ordinary income.

Consider the friction of that moment. Arthur wanted to write a check for $10,000 to the hospice. To do that, he had to withdraw roughly $13,000 to cover the immediate tax hit. The IRS took its cut first. Then, even though he gave the remaining money to charity, the inflated income bumped him into a higher tax bracket, triggering a chain reaction that increased the cost of his Medicare premiums.

He was being penalized for trying to do the right thing.

This is the invisible friction of American retirement. We are told to save, told to build, and told to support our communities. But the plumbing of our financial system was built for accumulation, not benevolence. For millions of retirees, the act of giving becomes a logistical nightmare of tax brackets, provisional income calculations, and systemic resistance.

The Partition in the Tax Code

There is a strange double standard baked into the way America handles retirement accounts.

If Arthur had been a wealthier man with a different kind of account—an Individual Retirement Account, or IRA—his story would have been entirely different. For years, IRA owners over the age of $70 \frac{1}{2}$ have enjoyed a financial superpower known as the Qualified Charitable Distribution (QCD).

The mechanics of a QCD are beautifully simple. It allows an individual to instruct their IRA custodian to send money directly to a qualified charity. The money never touches the account holder's hands. Because it never hits their bank account, it never counts as adjusted gross income. It satisfies their Required Minimum Distribution (RMD)—the mandatory amount the government forces you to withdraw each year once you hit 73—without pushing them into a crushing tax bracket.

It is a clean, elegant bypass.

Yet, for the vast majority of working-class Americans, the 401(k) is the default vehicle for retirement. Employers match it. HR departments push it. It is the bedrock of corporate savings. As of recent estimates, everyday workers hold trillions of dollars in these employer-sponsored plans.

But under current law, that elegant bypass does not exist for a 401(k).

If a retiree wants to use their 401(k) for charity, they face a tedious, multi-step bureaucratic gauntlet. First, they must roll the 401(k) funds over into a newly created traditional IRA. This requires paperwork, phone calls with disinterested customer service representatives, signatures, and waiting periods. Only after the money settles in the new IRA can they initiate the direct charitable gift.

Many seniors simply look at the paperwork and give up. The administrative burden acts as a tax on aging, punishing those who lack the cognitive stamina or financial literacy to navigate the system.

The status quo creates a stark divide. The sophisticated investor with an active financial advisor easily maneuvers around the tax traps. Meanwhile, the retired schoolteacher or assembly line worker, whose wealth is locked entirely in their old company 401(k), is left to bleed cash to the IRS just to support their local food bank.

The Quiet Coalition in Washington

Fixing a structural flaw this specific rarely makes front-page news. It lacks the visceral drama of culture wars or geopolitical standoffs. But in the halls of Congress, a quiet realization has been taking root: the current system is actively choking off billions of dollars in potential charitable giving at a time when non-profits are struggling to survive.

A new bipartisan effort is attempting to tear down the wall between 401(k) plans and direct giving.

The legislative push, championed by an unexpected alliance of lawmakers from both sides of the aisle, aims to harmonize the rules. The core proposal is straightforward: allow 401(k), 403(b), and 457(b) plan participants to execute the same direct, tax-free charitable distributions currently reserved for IRA holders.

Think about the immediate ripple effect of this change.

[Traditional 401(k) Withdrawal] ──> Retained Income Tax ──> Higher Tax Bracket ──> Reduced Charity Check

[Proposed Direct 401(k) Gift] ───────────────────────────────────────────────> Full Value to Charity

If the bill passes, a retired nurse with a 403(b) account could log into her retirement portal, click a button, and send $5,000 directly to an animal shelter or a university research fund. The money moves seamlessly. No rollover required. No artificial spike in income. No surprise spike in her Medicare Part B premiums the following year.

For the charities themselves, the stakes are immense. Non-profits operate on razor-thin margins, highly vulnerable to inflation and shifting economic winds. When a donor faces a tax penalty for giving, they give less. By removing the friction from 401(k) withdrawals, Washington would effectively unlock a massive, stagnant reservoir of capital, directing it straight into community organizations without costing the taxpayer a dime in direct federal spending.

It is rare to find a policy proposal where the incentives align so cleanly. It benefits the retiree who wants simplicity, the charity that needs funding, and the communities that rely on those charities to fill the gaps that government programs leave behind.

The Behavioral Friction of Giving

To understand why this change matters so deeply, we have to look past the numbers and examine human psychology. Human beings are profoundly sensitive to friction. If an action requires three steps instead of one, the likelihood of completing that action drops precipitously.

Imagine you are seventy-four years old. You are living on a fixed income. You want to support a local initiative to rebuild a community park. You call your 401(k) provider. They tell you that you cannot send the money directly. They tell you that you must open an IRA elsewhere, initiate a trustee-to-trustee transfer, wait two to four weeks, verify the transfer, and then request a check.

The momentum dies. The impulse to do good is swallowed by the dread of administrative minutiae.

The true cost of the current law isn't just measured in the tax dollars extracted from generous seniors. It is measured in the unwritten checks, the unfunded soup kitchens, and the community projects that never get off the ground because the barrier to entry was just a few inches too high.

We have built a culture that worships the accumulation of wealth but complicates its distribution. We celebrate the compounding interest of the 401(k) during a worker's career, but when that worker reaches the end of their life and decides they have enough, the system treats their generosity as a transactional anomaly that needs to be regulated and taxed.

Arthur Vance eventually did the rollover. He found a younger relative to help him navigate the online portals, fill out the forms, and move his hard-earned savings from his corporate 401(k) into a traditional IRA. It took him nearly two months of phone calls and verified signatures.

He finally wrote the check to the hospice center. It was a victory, but it was a exhausting one.

A few weeks later, Arthur sat on a bench in the hospice's garden, looking at a small brass plaque bearing his late wife’s name. The air was cool, the sky a bruised twilight gray. He was proud of what he had done, but he couldn't shake the memory of the bureaucratic maze he had to survive just to honor Martha's memory.

The law should not require a person to fight through an administrative thicket just to be kind. Generosity in the winter of life should be as simple as a single keystroke, allowing the wealth built over a lifetime of labor to flow directly to the places that need it most, unburdened by the cold calculations of an outdated tax code.