The headlines are screaming about a 3% inflation floor as if the sky is falling. They point at the geopolitical friction in the Middle East and the Federal Reserve’s "sticky" data points with a sense of impending doom. They are wrong. Most analysts are staring at the dashboard while the engine has already been swapped for a different model.

Stop waiting for 2%. It isn't coming back, and more importantly, we don't actually want it to.

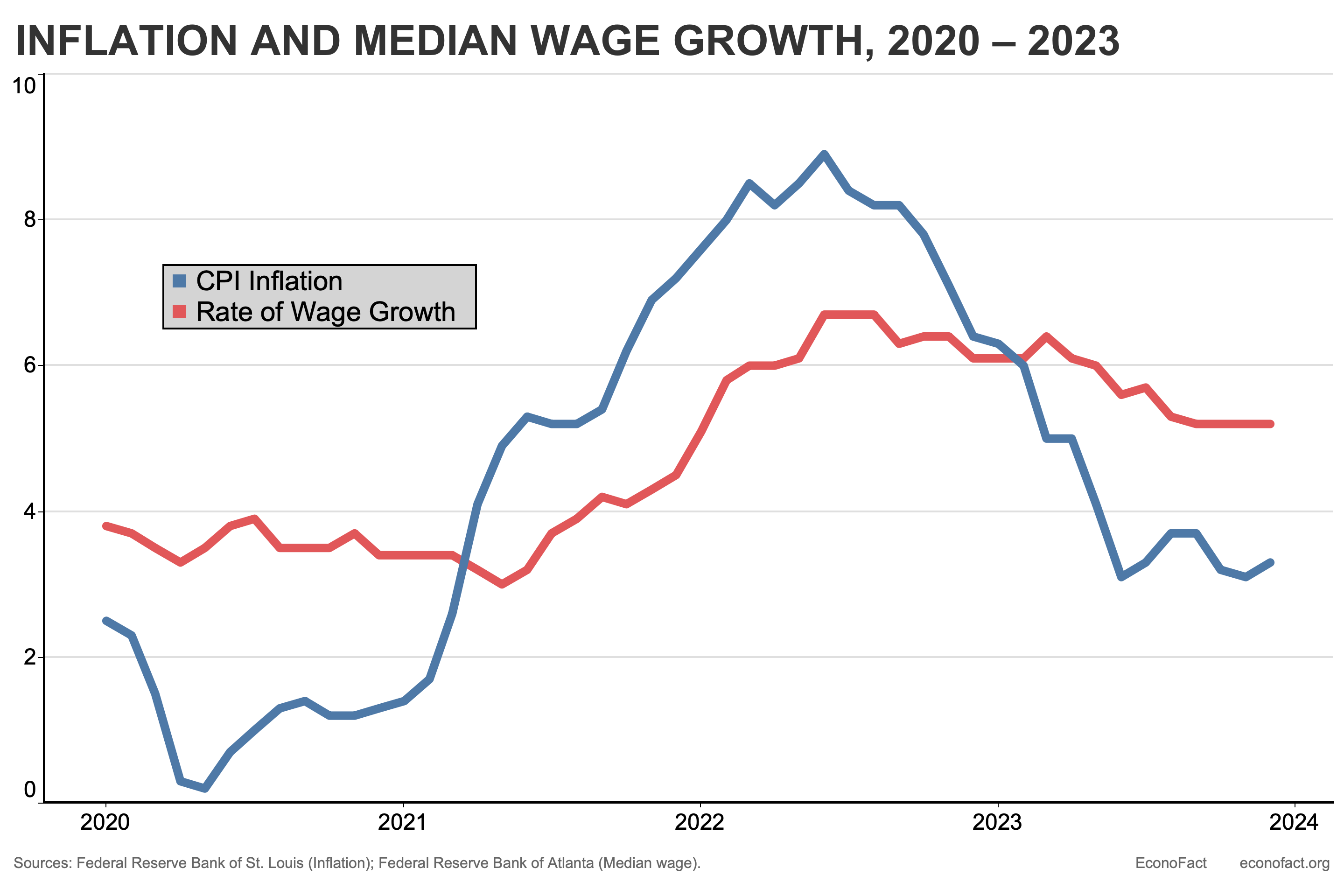

The obsession with a round number established in the 1990s is a relic of a dead era. We are currently witnessing the birth of a structural shift where 3% is the new neutral. If you are managing a portfolio or a business based on the "reversion to the mean" of the last decade, you are essentially betting on a ghost.

The Myth of the "Sticky" Metric

The media loves the word "sticky." It implies that inflation is a stubborn stain that just needs enough detergent—in this case, interest rate hikes—to disappear. This narrative assumes the current price pressure is a temporary malfunction of the supply chain or a byproduct of war-related oil spikes.

It isn't.

What we are seeing is the bill coming due for three decades of outsourced deflation. For years, the U.S. exported its inflation to developing markets by chasing cheap labor. That trade is over. Near-shoring, the green energy transition, and a shrinking global labor pool are inflationary by design. You cannot rebuild a domestic industrial base and keep prices at "Made in 2010" levels.

The Federal Reserve knows this. They won't admit it publicly because their credibility rests on the 2% mandate, but the quiet acceptance of 3% is a tactical surrender to reality.

War is a Distraction for Your Balance Sheet

The current conflict dynamics involving Iran are being used as a convenient scapegoat for the Fed's inability to hit its targets. Yes, energy prices spike during regional instability. Yes, shipping lanes get expensive when they become combat zones. But these are exogenous shocks. They are noise.

The real signal is the fiscal deficit.

We are running wartime deficits without a world war. When the government injects trillions into the economy through infrastructure bills and CHIPS Act subsidies, it creates a floor for demand that no amount of "tight" monetary policy can fully crush.

I’ve watched traders get liquidated trying to play the "peace dividend" every time a diplomatic cable leaks. They miss the point. Even if every missile in the Middle East stayed in its silo tomorrow, the structural demand for capital and the rising cost of labor would keep that 3% floor firmly in place.

The Fed’s Secret Best Friend

Why would the powers that be secretly enjoy 3% inflation?

Debt.

The United States is sitting on a mountain of sovereign debt that is mathematically impossible to pay back in "hard" dollars. The only way out is to inflate the currency. By keeping inflation slightly above the interest rate on that debt, the government effectively erodes the real value of what it owes.

If inflation drops to 1% or enters deflation, the debt-to-GDP ratio explodes, and the system collapses. They need inflation. They just need it to stay low enough that you don't start bartering for eggs. 3% is the "Goldilocks" zone for a bankrupt superpower.

Stop Asking if Rates Will Drop

The "People Also Ask" section of every financial site is littered with one question: "When will the Fed cut rates back to zero?"

The answer is: Hopefully never.

The era of free money—the ZIRP (Zero Interest Rate Policy) years—was a historical anomaly that distorted every asset class. it created "zombie companies" that only existed because their cost of capital was lower than their breath. It forced retirees into risky tech stocks because bonds paid nothing.

A 3% inflation environment with 4.5% or 5% interest rates is actually a healthy, functioning economy. It forces discipline. It means a business actually has to provide value to survive rather than just outrunning the printing press.

If you are waiting for a return to 2015, you are holding your breath until you turn blue. The "sticky" 3% isn't a failure of policy; it is the new baseline for a world that has stopped pretending that globalization is free.

The Strategy for the New Baseline

If you accept that 3% is the floor, your entire financial playbook changes.

- Abandon the 60/40 Portfolio: The old math of balancing stocks and bonds was built for a low-inflation, falling-rate world. In a 3% floor world, bonds aren't a hedge; they are a slow-motion leak.

- Pricing Power is the Only Metric: If you own a business or invest in one, check if they can raise prices by 5% tomorrow without losing half their customers. If the answer is no, that company is a casualty of the new regime.

- Hard Assets Over Hopes: Software-as-a-Service (SaaS) companies with no path to profit are yesterday’s news. Commodities, energy infrastructure, and specialized real estate are where the value stays when the currency is losing 3% of its bite every twelve months.

We are told that 3% is a "miss" by the Fed. In reality, it is the only thing keeping the gears of the modern economy from grinding to a halt under the weight of its own debt.

The "war" isn't with Iran or with "sticky" prices. The war is between the reality of a changing global economy and the fantasy of 2% stability that the media refuses to let go of.

Stop mourning the 2% target. It was a beautiful lie that we can no longer afford to tell.

Accept the 3%. Price it in. Move on.